A practical guide to understand spouse transfer, parent-child love and affection transfer, nominal RM10 stamping, RM1 million exemption, 50% remission and hidden costs before transferring property.

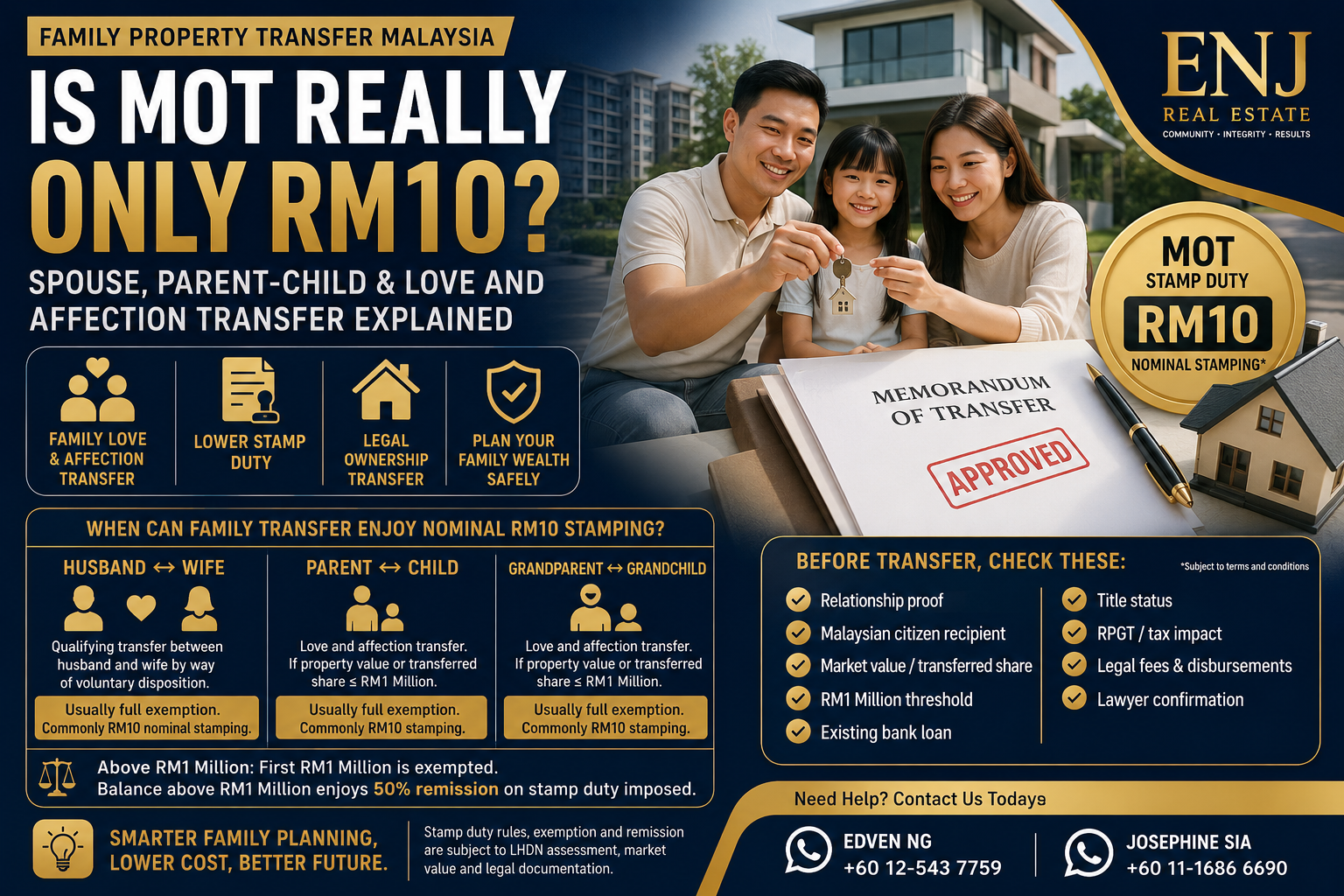

Yes, some family property transfers in Malaysia can be commonly understood as “RM10 MOT” or nominal RM10 stamping, but it depends on the relationship, property value and transfer structure.

For qualifying property transfer between husband and wife by way of voluntary disposition / love and affection, MOT stamp duty may be fully exempted. In practice, many buyers refer to this as nominal RM10 stamping, but legal fees, bank consent, refinancing cost and disbursement may still apply.

For qualifying transfer between parent and child, or grandparent and grandchild, the first RM1 million of the property market value may be fully exempted from MOT stamp duty. If the transferred property value or transferred share is not more than RM1 million, the practical stamping cost is commonly understood as nominal RM10 love and affection stamping. If the market value exceeds RM1 million, the amount above RM1 million is still subject to stamp duty, but with 50% remission, subject to conditions such as the recipient being a Malaysian citizen.

Many people say “family transfer only RM10”. This is only partly correct. RM10 is usually a practical way buyers describe a fully exempted instrument, not a rule that applies to every family transfer and every property value.

MOT stands for Memorandum of Transfer. It is the legal instrument used to transfer ownership of a property from one party to another.

In a normal property purchase, MOT stamp duty is usually calculated based on property value. But for certain family transfers, Malaysia provides stamp duty exemption or remission when the transfer is made under qualifying family relationships, usually by way of voluntary disposition / love and affection.

Before understanding RM10 love and affection transfer, buyers should understand the normal MOT stamp duty calculation.

| Property Value Band | Normal Stamp Duty Rate | Simple Explanation |

|---|---|---|

| First RM100,000 | 1% | First layer of property value. |

| Next RM400,000 | 2% | From RM100,001 to RM500,000. |

| Next RM500,000 | 3% | From RM500,001 to RM1,000,000. |

| Above RM1,000,000 | 4% | Any amount above RM1,000,000. |

For a RM1,200,000 property, normal MOT stamp duty would be approximately RM32,000:

RM1,000 + RM8,000 + RM15,000 + RM8,000 = RM32,000.

| Family Relationship | Common Practical Understanding | Important Limit |

|---|---|---|

| Husband ↔ Wife | Usually full MOT stamp duty exemption, commonly described as nominal RM10 stamping. | Legal fees, bank consent, refinancing and disbursements may still apply. |

| Parent ↔ Child | If qualifying transfer value is RM1 million or below, commonly described as nominal RM10 love and affection stamping. | If above RM1 million, the balance above RM1 million is still subject to stamp duty with 50% remission. |

| Grandparent ↔ Grandchild | If qualifying transfer value is RM1 million or below, commonly described as nominal RM10 love and affection stamping. | Recipient must be Malaysian citizen and conditions must be met. |

| Sibling / Uncle / Aunt / Cousin / Other Relatives | Usually not under the same exemption category. | Normal MOT stamp duty may apply. Always confirm with lawyer. |

Spouse transfer: Usually full MOT stamp duty exemption, commonly understood as nominal RM10 stamping.

Parent-child / grandparent-grandchild transfer: If RM1 million or below, commonly understood as nominal RM10 love and affection stamping. If above RM1 million, first RM1 million exempted and the balance gets 50% remission.

Sibling / other relatives: Usually no same exemption. Normal MOT stamp duty may apply.

For qualifying property transfer between husband and wife, stamp duty relief is generally more favourable. The MOT stamp duty may be fully exempted for an instrument of transfer of immovable property made between spouses by way of voluntary disposition.

Because the ad valorem MOT stamp duty is fully exempted, many lawyers, agents and buyers commonly explain it in simple terms as “only RM10 stamping”. However, this does not mean the entire transfer is free.

| Transfer Type | Common MOT Treatment | Buyer-Friendly Meaning |

|---|---|---|

| Husband to wife | Full MOT stamp duty exemption may apply. | Commonly understood as nominal RM10 stamping, subject to proper legal structure. |

| Wife to husband | Full MOT stamp duty exemption may apply. | Useful for family ownership restructuring or estate planning. |

| Adding spouse name to existing property | Depends on how the transfer is structured. | Lawyer must check title, loan, bank consent and whether it qualifies. |

Even if MOT stamp duty is exempted, the transfer may still involve legal fees, disbursement, valuation, bank consent, loan settlement or refinancing.

This is the part many buyers misunderstand. For parent-child property transfer in Malaysia, people often say “love and affection transfer only RM10”. This can be correct in practical terms when the transfer qualifies for exemption and the property value or transferred share is within the exempted threshold.

For qualifying transfer between parent and child, child and parent, grandparent and grandchild, or grandchild and grandparent, the first RM1 million of the property’s market value may be fully exempted from stamp duty. If the value is not more than RM1 million, buyers commonly understand the stamping as nominal RM10.

If the property market value is more than RM1 million, the first RM1 million may be exempted, but the balance above RM1 million is still subject to stamp duty with 50% remission.

| Family Transfer Type | Market Value / Transferred Share | Practical MOT Stamp Duty Treatment | Important Condition |

|---|---|---|---|

| Parent to child | RM1 million or below | Fully exempted. Commonly referred to as nominal RM10 love and affection stamping. | Recipient must be Malaysian citizen. |

| Child to parent | RM1 million or below | Fully exempted. Commonly referred to as nominal RM10 love and affection stamping. | Recipient must be Malaysian citizen. |

| Grandparent to grandchild | RM1 million or below | Fully exempted. Commonly referred to as nominal RM10 love and affection stamping. | Recipient must be Malaysian citizen. |

| Parent to child / grandparent to grandchild | Above RM1 million | First RM1 million exempted. Balance above RM1 million enjoys 50% remission on stamp duty imposed. | Recipient must be Malaysian citizen. |

| Sibling to sibling | Any value | No same family relief. Normal ad valorem MOT stamp duty usually applies. | Check with lawyer. |

Assume a parent transfers a property with market value of RM800,000 to a Malaysian citizen child by way of love and affection.

| Item | Normal Transfer | Parent-Child Love & Affection Transfer |

|---|---|---|

| Market value | RM800,000 | RM800,000 |

| Normal MOT stamp duty | Approx. RM18,000 | Exempted because within first RM1 million threshold |

| Practical stamping | Normal ad valorem duty applies | Commonly understood as nominal RM10 love and affection stamping |

This is why many people say parent-child love and affection transfer is “RM10”. But the statement is only safe when the transfer qualifies and the transferred value is RM1 million or below.

Assume a parent transfers a property with market value of RM1,200,000 to a Malaysian citizen child by way of love and affection.

| Item | Normal Transfer | Parent-Child Love & Affection Transfer |

|---|---|---|

| First RM1,000,000 | Normal MOT duty up to RM1 million = RM24,000 | Fully exempted |

| Balance RM200,000 | 4% × RM200,000 = RM8,000 | 50% remission, estimated payable RM4,000 |

| Estimated MOT Stamp Duty | RM32,000 | Approx. RM4,000, subject to LHDN adjudication and lawyer confirmation |

If the parent-child transfer value is RM1 million or below, many people describe it as “only RM10 love and affection stamping” because the MOT stamp duty is fully exempted. But once the property value exceeds RM1 million, it is no longer simply RM10 for the full transfer.

No. RM10 stamping does not mean the whole transfer is free. It usually only refers to the practical stamping treatment when the ad valorem MOT stamp duty is fully exempted.

| Cost Item | Still Need To Check? | Why It Matters |

|---|---|---|

| Legal fees | Yes | Lawyer still needs to prepare transfer documents, adjudication and registration. |

| Disbursement | Yes | Searches, registration, printing and other administrative costs may apply. |

| Bank consent | Yes | If the property is still under loan, bank approval or refinancing may be needed. |

| Valuation / market value | Yes | LHDN may assess stamp duty based on market value. |

| RPGT / tax | Yes | Transfer may have tax implications depending on facts and timing. |

| State consent / restrictions | Sometimes | Leasehold property, foreign interest, bumiputera lot or restriction-in-interest may require extra checks. |

Do not tell clients “family transfer confirm only RM10” without checking value, relationship, citizenship, title status, loan status and lawyer advice.

| Check Item | Why It Matters |

|---|---|

| Relationship proof | Birth certificate, marriage certificate or adoption document may be needed to prove eligibility. |

| Recipient citizenship | For parent-child and grandparent-grandchild relief, the recipient must be Malaysian citizen. |

| Market value / transferred share | The RM1 million threshold should be read based on the value being transferred and LHDN assessment. |

| Existing housing loan | If the property is still under bank loan, bank consent, discharge, assignment or refinancing may be needed. |

| Title status | Individual title, strata title, master title or assigned property may involve different documentation process. |

| RPGT / tax impact | Transfer may have tax implications. Always check with lawyer or tax advisor. |

| Future sale strategy | The new owner’s acquisition date and cost base may affect future disposal planning. |

RM10 is commonly used to describe fully exempted cases, but not every family relationship or value qualifies.

For parent-child and grandparent-grandchild transfer, the first RM1 million may be exempted, but the excess value still matters.

If the property is still financed, the bank has an interest in the property. Transfer cannot be treated like a simple name change.

Sibling-to-sibling, uncle-to-nephew, cousin-to-cousin or unrelated transfers may not enjoy the same relief.

LHDN may assess stamp duty based on market value, not a low declared transfer value.

Family transfer should be handled by a conveyancing lawyer to avoid wrong structure and unexpected costs.

For Johor Bahru buyers, family transfer planning is becoming more relevant because property prices, stamp duty and financing cost can affect family affordability.

Some families may choose to transfer an existing property to spouse or child. Others may prefer to buy a new property jointly from the beginning. For example, a couple buying a CIQ / RTS condo, landed home or second property should discuss ownership structure early before signing SPA.

Couples should decide whether to buy under one name or joint names based on loan, future transfer and ownership plan.

Parents and children should clarify ownership, contribution, future inheritance and transfer intention before purchase.

Existing property with title may be easier to plan for transfer, but loan and legal process must still be checked.

Foreign buyers or mixed-nationality families must check eligibility, state consent, stamp duty rate and legal ownership carefully.

Not always. It can be commonly understood as nominal RM10 stamping when the MOT stamp duty is fully exempted, such as qualifying spouse transfer or qualifying parent-child / grandparent-grandchild transfer within the RM1 million exemption threshold. Other cases may still attract stamp duty.

For qualifying property transfer between husband and wife by way of voluntary disposition, MOT stamp duty may be fully exempted. In practice, this is commonly referred to as nominal RM10 stamping, but legal fees, bank costs and disbursements may still apply.

It can be commonly understood as nominal RM10 love and affection stamping if the qualifying transfer value is RM1 million or below, because the MOT stamp duty on the first RM1 million may be fully exempted. If the property value exceeds RM1 million, the balance above RM1 million is subject to stamp duty with 50% remission, subject to conditions.

No. The relief generally applies only to specific family relationships such as husband and wife, parent and child, and grandparent and grandchild. Sibling-to-sibling, uncle-to-nephew, cousin-to-cousin or unrelated transfers generally do not enjoy the same relief.

For parent-child or grandparent-grandchild transfer under the current relief, the recipient must be a Malaysian citizen and the transfer must be by way of love and affection / voluntary disposition, subject to LHDN adjudication and lawyer confirmation.

No. Even if the MOT stamp duty is fully exempted, the family may still need to pay legal fees, disbursement, bank consent cost, refinancing cost, valuation fee or other related charges.

Reference Notes: This article is based on Malaysia stamp duty framework, LHDN / HASiL stamp duty guidance, Stamp Act 1949, P.U.(A) 420 spouse transfer exemption reference, and the 2023 love and affection transfer exemption for parent-child / grandparent-grandchild transfers. Actual eligibility, exemption, remission, nominal stamping, legal fees, RPGT and transfer process depend on signed documents, property title, market value, buyer profile, bank loan status and LHDN / lawyer assessment.

Before you buy, transfer or restructure property ownership, ENJ Real Estate can help you understand the difference between new purchase, joint ownership, spouse transfer, family transfer, RM10 MOT cases, love and affection transfer, and future resale planning.

WhatsApp Edven Ng: +60 12-543 7759

WhatsApp Josephine Sia: +60 11-1686 6690

Malaysia

Malaysia